1

City of Bellevue Tax Division

Guide to the City’s Business & Occupation Tax

January 1, 2024

This pamphlet provides a basic description

of Bellevue’s business and occupation (B&O)

tax and focuses on the more typical types

of businesses and business activities. The

material is intended for general information

purposes only. It is current at the time of

publication, but future changes in the city

code or state law may invalidate some of this

information, and not all possible applications

of tax are discussed.

Additional information and specics relating

to your business may be obtained in Chapters

4.03 and 4.09 of the Bellevue City Code or

by contacting the city’s Tax Division. Copies

of the code can be found online at Bellevue.

Municipal.Codes/BCC. The Tax Division can

be reached at:

phone: 425-452-6851

email: tax@bellevuewa.gov

website: BellevueWA.gov/tax

B&O TAX PAYMENT PROCEDURES

To conduct business in Bellevue, businesses

must register with the city and obtain a

Bellevue business license if they meet any of

the following criteria:

1. They have a physical location in the city, or

2. Their annual B&O taxable gross receipts in

the city will exceed $2,000 and they have

physical nexus in the City, or

3. They are subject to other taxes administered

by the city such as utility taxes.

You must still obtain all applicable regulatory

licenses and permits. If a regulatory license is

required, you will need to remit an application

with the appropriate addendums. A one-time

$113 general business license registration

fee is required. Register and le on-line at

FileLocal-WA.gov. A user and service fee

will apply. B&O tax returns or portal ling

reminders are sent to all taxpayers near the

end of each reporting period. Returns must

be completed and remitted with payment of

HIGHLIGHTS OF THE CITY’S

BUSINESS & OCCUPATION TAX

◼ All businesses registered to do business

with the city, whether located in the

city or located outside the city limits,

must report to the city based upon their

assigned reporting frequency even if no

tax is due.

◼ All businesses are subject to the

business and occupation (B&O) tax

unless specically exempted by Bellevue

City Code.

◼ B&O tax is due for businesses with

annual taxable receipts over $205,000.

◼ Businesses with annual taxable receipts

of $205,000 or less (and taxable square

footage of 250 square feet or less) will be

placed on an annual status.

◼ Current B&O tax rates:

f Gross receipts tax~ .1596% of gross

receipts

f Square footage tax~ $0.313286 per

square foot per quarter

2

any taxes due by the due date. Penalties and

interest are due if tax returns are not led

and taxes paid by the due date. Penalties and

interest are charged as follows:

Penalties

1 day –1 month overdue 9% ($5 min.)

over 1 month– 2 months 19% ($5 min.)

over 2 months 29% ($5 min.)

Annual interest rate for 2024 is 6%.

B&O TAX SCHEDULE

Quarterly multi-purpose tax return is due on

the following schedule:

Quarter Ending Payment Due

March 31 April 30

June 30 July 31

September 30 October 31

December 31 January 31

Helpful hints when submitting your

tax return

◼ File on-line at FileLocal-WA.gov to bypass

the next three bullet points. Fees may apply.

◼ Use the returns provided. Substitutions can

cause errors.

◼ Use the pre-addressed envelope provided

and add a return address.

◼ Make check or money order payable to City

of Bellevue. Do not send cash.

◼ Email the Tax Division of registration

changes such as address or status of

ownership changes to:

tax@bellevuewa.gov.

A tax return is due if a business is placed

on a ling status even if below Bellevue’s tax

exemption levels.

Taxpayers are required to keep records for

the most recent ve-year period. All books,

records, invoices, receipts, etc. shall be open

for examination at reasonable times by the

city’s Tax Division or designated agent.

COMPONENTS OF THE CITY’S B&O TAX

There are two components of the business

and occupation tax: gross receipts and square

footage. These B&O taxes support general

governmental services and the city’s Capital

Investment Program.

Every person, rm, association, or corporation

doing business in the city is subject to the

business and occupation tax. Some exemptions

are provided from the city’s B&O tax and will

be discussed later in this pamphlet. In general,

most businesses will report in the gross

receipts business tax category. A number of

businesses will report in the square footage tax

category. A limited number of businesses will

report in both categories.

GROSS RECEIPTS B&O TAX

The gross receipts B&O tax is primarily

measured on gross proceeds of sales or gross

income for the reporting period. For purposes

of the gross receipts tax, businesses have

been divided into several classications which

are discussed below. Businesses conducting

multiple activities will report in more than one

tax classication. The current gross receipts

tax rate of .1596% applies to all gross receipts

tax classications. As an example, for each

$100,000 in gross receipts, $159.60 tax is due.

Gross receipts tax classifications:

◼ Manufacturing/Processing for Hire

Manufacturing is the business of producing

articles for sale from raw or prepared

materials by giving these materials new

forms or qualities, such as fabricating,

processing, rening, mixing, packing,

canning, etc. B&O tax is calculated on the

value of products manufactured, determined

by selling price. Processing for hire means

the performance of labor and mechanical

services upon materials or ingredients

belonging to others so that as a result a new,

dierent or useful product is produced for

sale or commercial or industrial use. B&O

tax is calculated on gross receipts.

3

◼ Extracting/Extracting for Hire

Extracting is the taking of natural products,

such as logging, mining, quarrying, etc. B&O

tax is calculated on the value of products

extracted, determined by selling price.

Extractor for hire means a person who

performs under contract necessary labor or

mechanical services for an extractor. B&O

tax is calculated on gross receipts.

◼ Wholesaling

Sellers of products to persons other than

consumers are considered to be wholesalers.

The B&O tax is calculated on the wholesale

selling price.

◼ Retailing/Retail Service

Businesses that sell products and specic

services to consumers are dened as

retailers. Taxable retail services include

those generally performed on property, such

as repair, but not personal or professional

services, such as services performed by

doctors, attorneys, or accountants. The B&O

tax is calculated on gross receipts.

◼ Printing/Publishing

Publishers of newspapers, magazines

and periodicals are taxable under this

classication, as well as persons who both

print and publish books, music, circulars,

etc. Printing includes letterpress, oset-

lithography, and gravure processes as well

as multigraph, mimeograph, autotyping,

and similar activities. B&O tax is calculated

on gross receipts. Firms engaging in

photocopying documents should report

under the Retailing classication.

◼ Services and Other Activities

Businesses that provide personal and

professional services, such as lawyers,

doctors, nancial institutions, real estate

brokers, insurance brokers and solicitors,

and accountants, are subject to the B&O tax

under this classication. Also, any business

that is not subject to another B&O tax

classication must report under this “catch-

all” category. B&O tax is calculated on the

gross receipts of the business.

Exemptions, deductions, and credit allowed

for certain business activities:

The following section discusses a number

of the most common exemptions from the

gross receipts tax and deductions allowed

for certain business activities or sources of

income. This discussion is not intended to

be all inclusive. If you have questions about

specic exemptions or deductions, please

contact the city’s Tax Division.

Deductions are to be included in the gross

receipts amounts and then deducted when

calculating the taxable amount on which

the gross receipts tax rate applies. The most

common exemptions and deductions are

listed below.

Common Exemptions

◼ Taxable gross receipts equal to or less than

$205,000 annually. If you report quarterly

or monthly under the period threshold, then

you need to reconcile at year-end to the

annual threshold.

◼ Manufacturing, selling or distributing motor

vehicle fuel.

◼ Liquor, beer, and wine sales.

◼ Sale, lease, or rental of real estate. However,

no exemption is allowed for license to use

real estate or for amounts received as

commissions.

◼ Insurance agents (brokers are subject to tax).

◼ Farm products or edibles raised, produced

or manufactured within the State of

Washington and sold by the farmer.

◼ Nonprot organizations holding Federal IRS

nonprot status under 26 U.S.C. Section

501(c)(3), (4), or (7), except with respect to

retail sales.

◼ Casual and isolated sales, such as an

accountant selling his or her oce furniture.

◼ Day care homes in residences.

4

Common Deductions

◼ Retail or wholesale sales delivered outside

of Bellevue.

◼ Cash discounts taken by customers.

◼ Credit losses or bad debts sustained

by sellers.

Credit

Multiple activities tax credit applies to persons

who engage in business activities that

are subject to tax under two or more tax

classications on the same revenues.

SQUARE FOOTAGE TAX

The square footage B&O tax was implemented

to tax support space of oces whose business

activities are not directly attributable to the

generation of gross receipts to such activity.

Generally, the tax applies to businesses that

perform administrative activities or activities

that support sales delivered to locations

outside the city. Examples of administrative

activities include, but are not limited to

accounting, payroll, human resources, legal,

and other activities that are of only indirect

support to the activity subject to the gross

receipts B&O tax.

If a business has both an administrative

oce and a sales oce that generates gross

receipts, they may need to report the gross

receipts reportable to Bellevue and both

square footage of the administrative oce

and the square footage of the sales oce that

supports sales delivered to locations outside

the city. This is true whether personnel

performing administrative activities share

oce space with those that generate gross

receipts or sit in separate oces in the city.

Examples of businesses that pay the tax

include headquarter oces and businesses

that make out-of-city sales.

The square footage B&O tax is reported

under the Square Footage Tax Classication

on the multi-purpose tax return and is

measured on the taxable oor area of oce

space computed to the nearest square foot.

The current square footage B&O tax rate is

$0.313286 per taxable square foot per quarter.

As an example, for each 1,000 square feet of

taxable oce space, $313.29 tax is due each

quarter. This rate is adjusted each January

based on the change in the Consumer Price

Index to reect the eects of ination or

deation on the local economy.

Exemptions and deductions:

◼ Oces with taxable square feet of 250 or

less (Exemption).

◼ Oces which support business activity, all

or a portion of which is taxed under one

of the gross receipts tax classications

(Deduction). For example, a retailer who

sells in Bellevue, as well as outside the city

Limits, may deduct the percentage of oce

space which has been taxed under another

classication as noted in the following

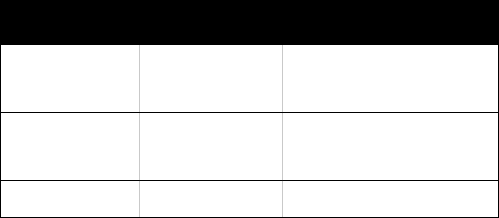

example:

Sales % of Total Sales

In-city

sales

$600,000 60% taxed

under Retailing

Out-of-city

sales

$400,000 40% deduction

under Retailing

Total sales $1,000,000 100%

40% of oce square footage is subject to the

square footage tax.

If a business has both an administrative oce

and a sales location which generates revenue

in Bellevue, they may need to report both the

square footage of the administrative oce and

the gross receipts and/or square footage of the

sales oce.

5

FAM-23-5702

OTHER TAXES AND LICENSES

There are several other taxes and regulatory

licenses that are administered by the city

which aect businesses in Bellevue. Following

is a brief synopsis of the additional taxes and/

or regulatory licenses that may apply to your

business:

Utility Tax: This tax is similar to the gross

receipts business and occupation tax except it

is imposed on utility businesses. The business

activities aected by this tax are telephone,

cellular, gas, electric, water, sewerage,

drainage, cable, and garbage. The rates range

from 4.5% to 10.4%.

Admission Tax: This tax is levied upon

persons who pay an admission charge for

entrance to an event or establishment. It is

collected for the city by the business charging

the admission, similar to the sales tax. The

admission tax is computed on the ticket price.

The rate is 3.0%.

Gambling Tax: All persons who are

licensed by the Washington State Gambling

Commission and conduct gambling activities

in the city are required to pay the gambling

tax. Such activities include bingo games,

raes, amusement games, and punchboards

& pulltabs. The rate ranges from 2.0% to 5.0%.

Regulatory Licenses: The following regulatory

licenses are administered by the Tax Division

and require annual renewal:

1. Ambulance Operator: Applies to

businesses which provide ambulance

services in Bellevue.

2. Dance Hall Operator and Premise: Applies

to the operator and premise where a public

dance is held for persons under twenty-

one years of age where no food or liquor is

served ($100/375).

3. Cabaret (music and dance): Applies to any

establishment which serves food or liquor

and where music, singing, dancing, or similar

entertainment is permitted ($400).

4. Adult Entertainment Cabaret: Applies to

any establishment open to the public where

adult entertainment is provided. Managers

and entertainers need an additional license

($700/$100).

5. Pawnbroker/Dealer: Applies to pawnbroker

activities and those dealing in precious

metals, stones or gems, jewelry, and bullion

($100).

6. Panoram: Applies to establishments which

charge for the display, viewing, or exhibition

of adult lms or video ($200).

7. Temporary Special Event: Applies to the

promoter of a special event where fteen

or more vendors are participating in the

selling, bartering, exchanging, trading, or

displaying of goods or services at an event

open to the public ($5 per day per vendor).

OTHER INFORMATION

All businesses should make every eort to be

fully informed of their tax liability, since the

nal responsibility for proper tax reporting

rests with the taxpayer. Failure to receive a

tax form does not relieve taxpayers of their

tax liability. Tax Forms are available on our

website at BellevueWA.gov/taxforms.

QUESTIONS?

If you have any questions, please visit the

Tax Division on our website at:

BellevueWA.gov/tax,

or Email: tax@bellevuewa.gov.

You may also write to the:

City of Bellevue Tax Division

P.O. Box 90012,

Bellevue, WA 98009-9012

or visit the Tax Division

Bellevue City Hall

450 110th Avenue NE

Phone: 425-452-6851

Fax: 425-452-6198

City of Bellevue

Tax Division

P.O. Box 90012

Bellevue, WA 98009-9012

For alternate formats, interpreters, or reasonable modication requests

please phone at least 48 hours in advance 425-452-6800 (voice) or email tax@

bellevuewa.gov. For complaints regarding modications, contact the City of Bellevue

ADA, Title VI, and Equal Opportunity Ocer at [email protected].

City of Bellevue Tax Division

Guide to the City’s Business & Occupation Tax

January 1, 2024