THE UNITED STATES

T

AX COURT

______

AN HISTORICAL ANALYSIS

Harold Dubroff & Brant J. Hellwig

Second Edition

Revised and Expanded

12/23/14 9:13 AM

i

PREFACE AND ACKNOWLEDGEMENTS

From the Original Edition:

The United States Tax Court has played a key role in the development

of Federal tax law since its founding as the Board of Tax Appeals in 1924.

For this reason, and because of its unusual procedures and judicial status,

we determined that it would be useful if a comprehensive study were

prepared dealing with the history and evolution of the Court. To this end a

grant was arranged to permit Professor Harold Dubroff of Albany Law

School to undertake the project. Although members of the Court reviewed

Professor Dubroff’s manuscript from time to time, the content of the study

is solely the responsibility of Professor Dubroff and should not be taken to

reflect the views of the Court or any of its Judges.

Work on the Tax Court project was commenced in 1974 and concluded

in 1977. As the various parts of the study were completed, they were

published in the Albany Law Review. * * *

We believe that the study is an important piece of scholarly work which

will be useful to both the Tax Court and the public in providing insight into

the forces which created and shaped the Court, its procedures and its

jurisdiction. We appreciate the efforts of the Albany Law Review in

publishing the study and permitting Commerce Clearing House, Inc. to

photocopy its issues, thereby making possible a wide public distribution at a

modest cost.

C. Moxley Featherston, Chief Judge

United States Tax Court

Howard A. Dawson, Jr. Judge

United States Tax Court

Washington, D.C.

1979

The concept of a history of the United States Tax Court largely came

from Judge Howard A. Dawson, Jr., then Chief Judge, and I wish to

express my gratitude to him for the suggestion that I undertake the project

and for the continuing help and support he furnished me as the work

progressed. Without his involvement, this study would not have been

possible.

ii

Other judges of the Court have also furnished their assistance during the

course of the work, and I wish to acknowledge my gratitude to them as

well. In particular, I would like to thank Chief Judge Moxley Featherston,

who made completion of the study possible, and Judge Charles R. Simpson,

who gave unstintingly of his time in reviewing manuscripts. Additionally,

Judge Bolon B. Turner, who served as a member of the Board of Tax

Appeals, and later as a judge of the United States Tax Court from 1937 to

1971, was of great assistance in providing me with valuable insights into

events which transpired during his long and productive tenure.

With respect to the research and writing of the book, several former

students provided valuable research assistance. Joseph R. Cook and Dan S.

Grossman deserve special thanks for their part in the preparation of Parts

V, VI, and VII [of the original edition.] Other former students whom I

wish to thank are Chris Boe, Judith L. Needham, and Kim Oster.

This book was originally published in six separate issues of the Albany

Law Review, and I am grateful for the editorial assistance provided by three

generations of law review members. My association with former Editor-in-

Chief Joseph H. Reynolds and former Managing Editor Gary Centola is one

which I will not soon forget.

Finally, I would like to thank my secretary, Iris Baum, whose persistent

good humor and cooperative spirit in the face of innumerable drafts and

redrafts were a constant source of wonder to me.

Harold Dubroff

Albany, New York

1979

Second Edition:

Following the publication of the original edition of this text, Professor

Dubroff published supplemental articles in the Albany Law Review that

brought the Tax Court study current to 1988. The original and

supplemental articles authored by Professor Dubroff represent a unique

source of detailed information about the Tax Court’s history and the

development and expansion of the Tax Court’s jurisdiction. In 2010, the

Court concluded that it would be appropriate to undertake a

comprehensive update of Professor Dubroff’s original work in this field.

Accordingly, the Court arranged for Professor Brant Hellwig of the

Washington and Lee University School of Law to draft the second edition

iii

of the text. The second edition updates the material originally authored by

Professor Dubroff and addresses important developments at the Tax Court,

including the considerable expansion of the Court’s jurisdiction subsequent

to the publication of Professor Dubroff’s work.

Work on the second edition commenced in 2010 and concluded in

2013. As a general matter, the second edition strives to bring the material

current to the beginning of 2013. The content of the revised text is solely

the responsibility of Professor Hellwig and should not be taken to reflect

the views of the Court or any of its Judges.

The Court appreciates the willingness of Professor Dubroff, Albany

Law Review, and CCH to graciously release any claim to the copyright so

that the second edition could be undertaken.

Michael B. Thornton, Chief Judge

United States Tax Court

John O. Colvin, Judge

United States Tax Court

Washington, D.C.

2014

Judge John O. Colvin, then Chief Judge of the United States Tax Court,

approached me in 2009 with an exciting albeit daunting proposition:

updating the seminal text authored by Professor Dubroff on the Tax

Court’s historical origins and its evolution as a court. I accepted, and the

second edition of the text is the product of that effort. The original

manuscript understandably served as a valuable source of information

about the Tax Court, and it is an honor to bring the text in line with more

recent developments.

The second edition leaves largely intact the first four Parts of the

original text, which provide a remarkably detailed history of the creation of

Board of Tax Appeals through the congressional chartering of the United

States Tax Court as a court of record established under article I of the

Constitution. Part V is a new chapter devoted to the judicial consideration

of the Tax Court’s constitutional status that culminated in the Supreme

Court’s 1991 decision in Freytag v. Commissioner.

Whereas the original text addressed procedural matters following the

discussion of the historical development of the Court, the second edition at

iv

this point turns to an examination of the Court’s jurisdiction. This portion

of the text represents the largest source of new material. In addition to

incorporating various aspects of the supplemental articles authored by

Professor Dubroff in the 1980s, the second edition details the numerous

ways in which Congress has expanded the Tax Court’s jurisdiction in recent

times. Whereas the original text devoted a single, lengthy chapter to the

Tax Court’s jurisdiction, the second edition breaks this material into three

chapters. Part VI addresses foundational aspects of the Court’s jurisdiction,

such as its deficiency and refund jurisdiction. Part VII examines a number

of innovations in the Tax Court’s jurisdiction that, broadly speaking, are

intended to improve the efficiency of tax litigation. Lastly, Part VIII

explores the jurisdiction of the Tax Court to review the administration of a

variety of recently created taxpayer rights.

Following the examination of the Tax Court’s jurisdiction, the second

edition turns to a discussion of Tax Court procedure. Part IX is devoted to

pretrial matters, Part X to trial procedure, and Part XI to post-trial

considerations. Part XII is a new chapter devoted to the position of the

Special Trial Judge. Part XIII concludes by addressing the various means

by which the Court provides institutional support to self-represented

taxpayers.

In the course of this project, I have received considerable support from

several of the Court’s Judges and members of its professional staff. I

greatly appreciate the encouragement and guidance I have received from

Chief Judge Michael B. Thornton and Judge John O. Colvin. I wish to

extend a particular note of gratitude to Special Trial Judge Daniel A. Guy,

Jr. In addition to generously devoting his time in reviewing drafts of the

manuscript, he largely oversaw the project on behalf of the Court. Andrea

Blake and Audrey Nutt of the Court’s staff devoted significant effort to this

project by providing drafts of updates on discrete topics, and I greatly

appreciate their contributions.

Additionally, I am grateful for the research assistance I received from

law students over the years I worked on this project. One former student,

Christopher Hines, significantly improved the text through his editorial

efforts. As a final matter, I commenced work on this project while a

member of the Law School faculty at the University of South Carolina and

concluded it while a member of the Law School faculty at Washington and

Lee University. I thank both institutions for their support.

Brant J. Hellwig

Lexington, Virginia

2014

v

THE UNITED STATES TAX COURT

AN HISTORICAL ANALYSIS

TABLE OF CONTENTS

PART I

O

RIGINS OF THE TAX COURT ........................................................................... 1

A. Development of the Income Tax ............................................................... 1

B. Inadequacy of Preexisting Adjudicative Institutions .............................12

1. Dilemma of the Bureau ......................................................................13

2. The Judicial Remedy ...........................................................................29

3. Pre-Assessment Review Within the Bureau ....................................38

P

ART II

C

REATION OF THE BOARD OF TAX APPEALS:

T

HE REVENUE ACT OF 1924 ............................................................................49

A. The Revenue Act of 1924 ..........................................................................49

B. The Administration Proposal for a Board of Tax Appeals ..................53

C. Controversy and Modifications ................................................................57

1. Independence .......................................................................................58

2. Procedure ..............................................................................................63

3. Personnel ..............................................................................................70

4. Jurisdiction ............................................................................................76

5. Effect of Board Decision ...................................................................81

D. The Board from 1924–1926 ......................................................................84

1. Selection of Members .........................................................................86

2. Rules of Practice and Procedure .......................................................93

3. The Board in Operation .................................................................. 102

4. Success of the Board ........................................................................ 108

P

ART III

T

HE REVENUE ACT OF 1926:

I

MPROVING THE BOARD OF TAX APPEALS .............................................. 115

A. The Revenue Act of 1926 ....................................................................... 115

B. Status of the Board .................................................................................. 117

C. Appeals and Finality ................................................................................ 122

D. Jurisdiction ................................................................................................ 131

1. Exclusivity of Board Jurisdiction ................................................... 131

2. Effect of Payment and Limited Refund Jurisdiction .................. 133

vi

3. Jeopardy Assessments ...................................................................... 136

E. Members .................................................................................................... 140

1. Number of Members ....................................................................... 141

2. Compensation of Members ............................................................ 144

3. Tenure of Members ......................................................................... 146

4. Removal of Members ...................................................................... 151

5. Restrictions on Practice ................................................................... 152

6. Background of Members ................................................................. 155

F. Practice and Procedure ........................................................................... 159

G. Division Decisions and Expediting the Board’s Workload .............. 163

H. Conclusion ................................................................................................ 170

P

ART IV

T

HE BOARD BECOMES A COURT ................................................................ 175

A. The Board of Tax Appeals from 1924 to 1942 ................................... 175

B. The Tax Court of the United States – An Independent Agency

in the Executive Branch of the Government ............................................ 185

1. The Revenue Act of 1942 – the Board of Tax Appeals is

Renamed the Tax Court of the United States .............................. 186

2. Attempts to Incorporate the Tax Court into the Federal Judicial

System ................................................................................................ 195

C. The United States Tax Court – A Court of Record Established Under

Article I of the Constitution ................................................................... 217

D. Questions Concerning Constitutional Status of the

Court’s Jurisdiction .................................................................................. 228

E. Proposals to Consolidate Tax Litigation Before the Tax Court ....... 232

F. Subsequent Developments Consistent With Judicial Status ............. 236

1. Court Security ................................................................................... 238

2. Tax Court Personnel System .......................................................... 238

3. Codes of Conduct and Public Disclosures .................................. 238

4. E-Government Act .......................................................................... 239

5. Admissions and Discipline ............................................................. 240

P

ART V

A

JUDICIAL EXAMINATION OF THE TAX COURT’S CONSTITUTIONAL

NATURE:

FREYTAG V. COMMISSIONER

.................................................... 241

A. Developments Before the Tax Court ................................................... 242

B. Decisions at the Courts of Appeals ...................................................... 247

C. The Supreme Court Decision ................................................................ 252

vii

D. Postscript ................................................................................................... 263

E. Conclusion ................................................................................................ 265

F. Subsequent Development: Kuretski v. Commissioner ............................ 266

P

ART VI

F

OUNDATIONAL PARAMETERS OF TAX COURT JURISDICTION ......... 269

A. Deficiency Jurisdiction ............................................................................ 271

1. Taxes Subject to the Tax Court’s Deficiency Jurisdiction ......... 272

2. Deficiency Jurisdiction: Procedural Requirements .................... 275

3. Jurisdiction to Restrain Premature Assessment and

Collection ........................................................................................... 298

B. Refund Jurisdiction .................................................................................. 301

1. Statute of Limitations on Overpayment Determinations .......... 304

2. Resolution of Potential Concurrent Overpayment

Jurisdiction ......................................................................................... 308

3. Authority to Order Refund of Overpayment .............................. 311

4. Proposals to Expand Refund Jurisdiction .................................... 315

C. Jeopardy Jurisdiction ............................................................................... 323

1. Jeopardy Assessments ...................................................................... 327

2. Termination Assessments ............................................................... 338

3. Review of Proposed Sale of Property Obtained Through

Jeopardy or Termination Assessment ........................................... 345

D. Scope of Judicial Powers......................................................................... 349

1. Enforcement Powers ....................................................................... 350

2. Power to Review Constitutionality of Laws ................................. 353

3. Equitable Powers .............................................................................. 357

P

ART VII

E

NHANCING THE EFFICIENCY OF TAX ADJUDICATION:

INNOVATION IN REMEDIES AND PROCEDURES ................................... 387

A. Declaratory Judgments ............................................................................ 387

1. Early Subjects of Declaratory Judgment Jurisdiction ................. 388

2. Expansions of Declaratory Judgment Relief ................................ 403

B. Review of Worker Classification Determinations .............................. 408

C. Innovations in Partnership Proceedings .............................................. 411

1. Uniform Partnership Proceedings Under TEFRA ..................... 412

2. Tax Treatment of Subchapter S Items .......................................... 433

3. Electing Large Partnership Provisions .......................................... 434

4. Declaratory Judgments Relating to “Oversheltered” Returns .. 438

viii

D. Supplemental Tax Court Jurisdiction ................................................... 441

1. Post-Decision Interest Determinations ........................................ 442

2. Continuing Jurisdiction Over Estate Tax Cases .......................... 445

P

ART VIII

T

AX COURT PROMINENCE IN JUDICIAL REVIEW

OF TAXPAYER RIGHTS ................................................................................... 447

A. Disclosure Actions ................................................................................... 447

B. Relief from Spousal Joint and Several Liability ................................... 456

1. Relief Under Former Section 6013(e) ........................................... 458

2. Section 6015(b) Relief ...................................................................... 461

3. Section 6015(c) Relief ...................................................................... 464

4. Section 6015(f) Relief ....................................................................... 465

5. Procedure for Requesting Innocent Spouse Relief ..................... 466

6. Tax Court Jurisdiction ..................................................................... 468

7. Standard and Scope of Review ....................................................... 472

8. Rights of the Nonrequesting Spouse............................................. 474

C. Jurisdiction to Review Denials of Interest Abatement ...................... 475

D. Review of Determinations in Collection Due Process

Proceedings ............................................................................................... 481

1. The Government’s Summary Collection Powers ........................ 481

2. The Pre-Deprivation Administrative Hearing ............................. 483

3. Judicial Review .................................................................................. 488

E. Reimbursement of Taxpayer Litigation and Administrative Costs .. 502

1. Pre-TEFRA Rules ............................................................................ 503

2. Taxpayer Rights as Expanded by TEFRA ................................... 507

3. Tax Court Jurisdiction ..................................................................... 526

F. Review of Whistleblower Award Determinations .............................. 530

P

ART IX

P

RETRIAL PROCEDURE .................................................................................. 539

A. The Deficiency Notice ............................................................................ 541

B. The Petition .............................................................................................. 545

1. Content of the Petition .................................................................... 546

2. Congestion of Appeals .................................................................... 553

C. The Answer ............................................................................................... 565

1. Filing Requirements ......................................................................... 565

2. The General Denial .......................................................................... 572

3. Affirmative Allegations .................................................................... 578

ix

D. The Reply .................................................................................................. 585

1. Filing ................................................................................................... 586

2. Content and Form ............................................................................ 595

E. Stipulations ................................................................................................ 598

1. Stipulations from 1924 to 1945 ...................................................... 600

2. The 1945 Revision ............................................................................ 603

3. Putting Teeth into the Rule: 1955 Revision ................................ 605

4. Revisions of the 1960s ..................................................................... 606

5. 1974: Rule 31(b) Becomes Rule 91 ............................................... 614

F. Pretrial Conferences ................................................................................ 617

G. Discovery................................................................................................... 623

1. Adoption of Discovery Procedures ............................................... 631

2. Expanding Discovery Techniques ................................................. 633

3. Discovery of Expert Witnesses ...................................................... 641

4. Restructuring and Expansion of Deposition Procedures .......... 648

5. Limitations on the Use of Interrogatories .................................... 649

6. Sanctions for Discovery Abuse ...................................................... 649

H. Case Management Procedures ............................................................... 656

1. Joint Motion for Assignment of a Judge ...................................... 656

2. Motions Practice ............................................................................... 656

3. Calendaring Cases for Trial ............................................................. 657

4. Standing Pretrial Order and Pretrial Memorandum ................... 658

5. Standing Pretrial Notice .................................................................. 662

6. Final Status Report ........................................................................... 663

I. Alternative Dispute Resolution ............................................................. 663

P

ART X

T

RIAL PROCEDURE ......................................................................................... 667

A. Place of Trial ............................................................................................. 668

B. Evidence .................................................................................................... 673

C. Burden of Proof ....................................................................................... 682

1. Development of General Rule ....................................................... 682

2. Fraud................................................................................................... 690

3. New Matter ........................................................................................ 694

4. Reassignment of Burden of Proof Pursuant to Section 7491 ... 699

D. Damages for Frivolous or Groundless Proceedings .......................... 706

1. Pre-TEFRA Damages ...................................................................... 706

2. Damages Expanded by TEFRA .................................................... 711

3. Subsequent Statutory Developments ............................................ 720

x

P

ART XI

O

PINIONS, DECISIONS, AND APPEALS ...................................................... 729

A. The Decision Process .............................................................................. 729

B. Development of the Single-Member Division Structure ................... 731

C. Findings of Fact and Opinion................................................................ 736

D. Bench Opinions ....................................................................................... 739

1. The Amendment of Section 7459(b) ............................................. 739

2. The Proposal of Rule 152 ............................................................... 743

3. The Adoption and Employment of Rule 152 .............................. 747

E. Memorandum Opinions ......................................................................... 750

F. Court Conference .................................................................................... 754

1. Historical Origins ............................................................................. 755

2. Voting Procedures ............................................................................ 760

3. 1985 Amendments to Conference Procedures ............................ 764

G. Rule 155 ..................................................................................................... 777

H. Appeals ...................................................................................................... 784

1. Federal Rules of Appellate Procedure ........................................... 784

2. Time for Filing Appeal .................................................................... 785

3. Effect of Motion to Vacate ............................................................. 787

4. Finality of Tax Court Decisions ..................................................... 788

5. Reviewable Decisions ...................................................................... 789

6. Venue.................................................................................................. 792

7. The Appellate Process in Operation—Problems and

Controversies .................................................................................... 800

8. Scope and Standard of Review ....................................................... 802

9. Precedential Value of Decisions of Other Courts ...................... 814

P

ART XII

S

PECIAL TRIAL JUDGES .................................................................................. 823

A. Historical Origins ..................................................................................... 823

B. Early Expansion in Use of Special Trial Judges .................................. 830

C. Authority to Make Decisions in Certain Cases ................................... 831

D. Review of Special Trial Judge Reports ................................................. 835

E. Examining the Tax Court’s Procedures for Reviewing Special

Trial Judge Reports: The Saga of Ballard v. Commissioner ................... 840

1. Analysis of Rule 183 Procedures in Freytag v. Commissioner ........ 843

2. The Initial Tax Court Opinion in Ballard ...................................... 851

3. Post-Trial Developments ................................................................ 853

4. Treatment at the Circuit Courts of Appeals ................................. 856

xi

5. Supreme Court Review .................................................................... 863

6. Release of the Initial Report of the Special Trial Judge ............. 871

7. Corrective Action ............................................................................. 875

8. Remand of the Proceedings to the Tax Court ............................. 876

9. The Tax Court’s Resolution of the Case on Remand ................. 878

10. The Unwelcomed Return to the Courts of Appeals ............... 879

11. Conclusion ..................................................................................... 881

P

ART XIII

T

HE SMALL TAX CASE PROCEDURE AND

S

UPPORT FOR SELF-REPRESENTED LITIGANTS..................................... 883

A. Small Tax Cases ........................................................................................ 883

1. Amount in Dispute .......................................................................... 887

2. Expansion in Scope of Small Tax Cases ....................................... 889

3. Election by the Taxpayer ................................................................ 891

4. Discontinuance ................................................................................. 894

5. Answers in Small Tax Cases ........................................................... 895

6. Pretrial Procedures ........................................................................... 896

7. Informal Procedures ........................................................................ 896

B. Court Measures to Support Self-Represented Taxpayers .................. 897

1. Taxpayer Information ...................................................................... 897

2. Low-Income Taxpayer Clinics ....................................................... 899

3. Bar Sponsored Calendar Call Programs........................................ 901

A

PPENDIX A

W

ORKLOAD OF BOARD OF TAX APPEALS AND

T

AX COURT 1925–2012 .................................................................................... 905

A

PPENDIX B

T

AX COURT CASELOAD BY TYPE (IN MODERN TIMES) ....................... 909

A

PPENDIX C

A

REAS OF FORMER TAX COURT JURISDICTION ..................................... 911

A. Renegotiation Cases ................................................................................. 911

1. Nature of Remedy ............................................................................ 915

2. Burden of Proof................................................................................ 916

3. Appellate Review .............................................................................. 919

B. Refunds of Processing Tax ..................................................................... 922

xii

APPENDIX D

L

OCATIONS OF TAX COURT HEARINGS .................................................... 925

A

PPENDIX E

S

TANDING PRETRIAL ORDER ...................................................................... 927

A

PPENDIX F

S

TANDING PRETRIAL NOTICE ..................................................................... 931

A

PPENDIX G

T

ECHNOLOGICAL DEVELOPMENTS AT THE COURT ............................ 935

A. The Tax Court Website ........................................................................... 935

B. Electronic Case Filing ............................................................................. 936

C. Electronic Courtroom ............................................................................. 937

D. Security and Privacy Protections ........................................................... 937

The Origins of the Tax Court 1

PART I

ORIGINS OF THE TAX COURT

As with most institutions, the Tax Court, which was created in 1924 as

the Board of Tax Appeals, originated in response to an existing need. In its

case the need was created by the combination of two factors. The first of

these was the development of the federal income and profits taxes and their

emergence during World War I as the preeminent devices for financing the

operations of Government. The second was the inadequacy of preexisting

institutions, both administrative and judicial, for adjudicating in an

acceptable manner the disputes growing out of the changed conditions

brought on by the new taxes.

A. Development of the Income Tax

Although the Tax Court has had other duties, the principal reason for its

creation was, and its main function has always been, the adjudication of

disputes involving the federal income and profits taxes.

1

For this reason,

the history of the court must start with the development and early history

of the modern income tax.

2

In present times, federal income taxes are of such a pervasive and

significant influence that it is easy to forget that these taxes did not exist for

1

In the course of its history, the Tax Court has also had jurisdiction to

redetermine deficiencies in estate and gift taxes, and excise taxes on foundations.

Additionally, for a period of almost three decades, it had jurisdiction to redetermine

excessive profits under the Renegotiation Acts. The jurisdiction of the Tax Court

is more particularly described in Parts VI through VIII.

2

Much of the material dealing with the development of the income tax and the

early administrative problems faced by the Bureau of Internal Revenue was derived

from secondary sources. These sources are identified below and, in general, will not

be cited further. B

ORIS I. BITTKER AND LAWRENCE M. STONE, FEDERAL INCOME,

ESTATE AND GIFT TAXATION (4th ed. 1972); ROY G. BLAKEY & GLADYS C.

BLAKEY, THE FEDERAL INCOME TAX (1940); BUREAU OF INTERNAL REVENUE,

T

HE WORK AND JURISDICTION OF THE BUREAU OF INTERNAL REVENUE (1948);

J

OHN C. CHOMMIE, THE INTERNAL REVENUE SERVICE (1970); LOUIS

E

ISENSTEIN, THE IDEOLOGIES OF TAXATION (1961); LAWRENCE M. FRIEDMAN,

A HISTORY OF AMERICAN LAW (1973); INTERNAL REVENUE SERVICE, INCOME

TAXES 1862–1962: A HISTORY OF THE INTERNAL REVENUE SERVICE (1962);

R

ANDOLPH E. PAUL, TAXATION IN THE UNITED STATES (1954); SIDNEY RATNER,

AMERICAN TAXATION (1942); 1 STANLEY S. SURREY, WILLIAM C. WARREN, PAUL

R. MCDANIEL & HUGH J. AULT, FEDERAL INCOME TAXATION (1972); Bolon B.

Turner, The Tax Court of the United States, its Origin and Function, in

THE HISTORY

AND

PHILOSOPHY OF TAXATION 31 (1955) [hereinafter cited as Turner].

2 The United States Tax Court – An Historical Analysis

much of the country’s history. The colony of New Plymouth had imposed

a rudimentary income tax as early as 1643 and other colonies and later some

states had made use of such taxes in the 17th and 18th centuries. However,

the first federal income tax was not imposed until the latter half of the 19th

century. Prior to that time, the small revenue needs of the Federal

Government were primarily satisfied by tariffs, although internal excise

taxes and the sale of public lands also played some part in financing the

Government.

The most important factor in the development of the income tax has,

unfortunately, been the financial exigencies attendant on the state of war.

Toward the end of the War of 1812, Alexander J. Dallis, Secretary of

Treasury, recommended enactment of an inheritance and income tax that

he thought could “be easily made to produce $3 million.” However, the

war ended before the proposal could be enacted and the following half-

century of relative peace resulted in little further attention being paid to

income taxation. That peace was shattered by the Civil War, which created

unprecedented revenue needs not capable of being fulfilled by traditional

techniques. Government expenditures jumped from $67 million in 1861 to

$475 million in 1862, $715 million in 1863, $865 million in 1864, and $1.3

billion in 1865, an increase of 19 fold in only five years.

3

During the war,

most revenue was raised by public debt financing, and budget deficits

amounted to more than two-thirds of the Union’s expenditures for the

years 1862–65.

The Government fell into such an unfortunate financial position as a

result of a combination of factors. First, the war had an unexpectedly high

cost because the Confederate armies proved to be a more formidable

adversary than the initially optimistic Union forces estimated. Second, the

Lincoln administration was not particularly adept in public finance. Many

years before his election, Lincoln himself conceded that he “had no money

sense” and did not “fret” over the subject. His Secretary of the Treasury

for the initial war years, Salmon P. Chase, was similarly ungifted. Chase’s

principal interests were in military and political affairs, and he relied heavily

on a noted financier of the day, Jay Cooke, to raise revenue through the sale

of government bonds. Finally, the United States since its inception had

been a country of low government expenditures and correspondingly low

taxes. By 1860 tax revenues had reached a high of only $56 million, and in

most prior years the budget was in surplus. Against this background,

neither the Congress nor the citizenry were well equipped to cope with

3

Statistical data contained herein was derived from the following sources:

C

OMM’R OF INTERNAL REVENUE, STATISTICS OF INCOME FOR 1941 pt. 1 at 270

(1945) (corporate return statistics, 1909–41); J

OINT ECONOMIC COMMITTEE, THE

FEDERAL TAX SYSTEM: FACTS AND PROBLEMS 1964, 88th Cong., 2d Sess. 214–15

(1964) (individual return statistics, 1913–61); 1962 T

REAS. ANN. REP., FINANCES,

508–15 (1963) (government receipts and expenditures 1789–1962).

The Origins of the Tax Court 3

financing the staggering new expenditures, which exceeded $2 million per

day for the war alone.

Nevertheless, the need for new and increased taxes soon became

painfully apparent since the major existing revenue source, tariffs, was

clearly inadequate to satisfy the revenue requirements. Some favored

supplementing tariffs only with direct taxes on real estate apportioned

among the states according to population, as required by the Constitution.

However, representatives of the Western states felt that this would unduly

favor the Northeast where it was thought there existed a heavier

concentration of wealth in proportion to population. In response to this

pressure, Congress adopted in 1861, and implemented in 1862, the first

federal income tax as part of a multi-faceted program of taxation.

4

This first income tax was a modest one. It exempted incomes below

$600, and taxed amounts above that level at a rate of only 3% from $600 to

$10,000 and at a rate of 5% on income above $10,000.

5

In its first year it

raised only $2.7 million as opposed to government expenditures for the year

of more than $700 million. Subsequently, as the need for revenues

mounted, the tax rates were increased. By 1865, the rates stood at 5% on

income from $600 to $5,000 and 10% on income above $5,000.

6

This was

to be the high water mark of income taxation for more than 50 years. With

the end of the Civil War the exemption was enlarged and the rates reduced,

and finally, effective in 1872, the income tax was repealed.

7

At no time did the Civil War income tax represent as significant a source

of government revenues as the modern day income taxes. The lowest yield

occurred in 1863 when $2.7 million was raised, and the highest yield

occurred in 1866 when $73 million was raised. This is to be contrasted with

total revenues in those years of $113 million and $559 million, respectively.

By 1872, the last year of the tax, its yield had declined to $14 million as

against total revenues of $374 million. But despite its relative unimportance

as a source of revenue, the income tax attracted a considerable amount of

attention during this period.

At the time of its adoption, the income tax was generally supported as a

necessary step in solving the financial needs of the war. The end of the war

4

Act of August 5, 1861, ch. 45, § 49, 12 Stat. 309; Act of July 1, 1862, ch. 119,

§ 89, 12 Stat. 473.

5

Act of July 1, 1862, ch. 119, § 90, 12 Stat. 473.

6

Act of March 3, 1865, ch. 78, 13 Stat. 479. In the interim between 1862 and

1865, the tax had been increased to 5% on income between $600 and $5,000, 7½%

on income between $5,000 and $10,000, and 10% on income in excess of $10,000.

Act of June 30, 1864, ch. 173, § 116, 13 Stat. 281.

7

Act of July 14, 1870, ch. 255, § 6, 16 Stat. 257. In 1867, the exemption was

increased to $1,000 and the rate reduced to 5%. Act of March 2, 1867, ch. 169,

§ 13, 14 Stat. 478. In 1870, the exemption was further increased and the rate further

reduced to $2,000 and 2½%, respectively. Act of July 14, 1870, ch. 255, §§ 6, 8, 16

Stat. 257–58.

4 The United States Tax Court – An Historical Analysis

and the reestablishment of regular surpluses of revenue over expenditures

brought increasing pressure for reduction and finally repeal of the tax.

Primarily, this pressure came from the banking and commercial interests of

the Northeast, which much preferred tariffs to income taxes since the

former had the double advantage of being taxes on consumption and

providing domestic products with a competitive advantage. The income tax

had its defenders who strenuously argued that taxation based exclusively on

consumption was unjust because it imposed disproportionately heavy taxes

on persons of lower income who by necessity consumed a higher

percentage of their income than persons with large incomes.

Despite these arguments, the anti-income tax forces prevailed essentially

because of their greater political power both as lobbyists and propagandists.

They argued that the tax was superfluous in periods of surplus, that it was

inequitable in many of its provisions, and that it necessitated the creation of

an inquisitorial enforcement bureaucracy which proved to be inefficient and

subject to political influence.

The quarter of a century following the repeal of the income tax was a

period of considerable social ferment in the United States. A severe

financial panic occurred in 1873 and was immediately followed by a

devastating depression. The farmers of the South and the West were

particularly hard hit during these years by declining prices for their products

with no corresponding decline in the prices they had to pay for supplies,

storage, and transportation. Economic power became concentrated in

banks, railroads, and various other industrial and commercial interests.

Against this background a strong agrarian and populist movement

developed to challenge the power of the Northeast. Among the important

objectives of these groups were cheap money, regulation or destruction of

the monopolies, and the imposition of an income tax.

Reinstitution of the income tax had been proposed by Southern and

Western congressmen throughout the post-Civil War period. It was not

until 1894, however, that a coalition of Populists and Southern and Western

Democrats succeeded in engineering its passage as part of a program to

reduce tariffs and tax the rich.

8

The measure was totally congressional in its

initiation and passage. President Cleveland, who favored reduced tariffs but

opposed passage of an income tax, allowed it to become law without his

signature.

The tax, which was miniscule by modern standards (2% of the income

of individuals and corporations, with an exemption of $4,000), was bitterly

opposed by the Eastern establishment, who viewed it as the opening salvo

in a class war of poor against rich. They found substantiation for their fears

in the new measure itself which exempted from tax all but the wealthiest 2

percent of the population, whereas under previous taxes this same group

paid only 2 percent of the total revenues generated. Moreover, if a 2% tax

8

Act of August 27, 1894, ch. 349, § 27, 28 Stat. 553.

The Origins of the Tax Court 5

on incomes above $4,000 could be imposed, nothing would prevent

imposition of a 20% tax on incomes above $40,000. It is not surprising,

therefore, that the rhetoric employed was extreme. In polite society the tax

was referred to as radical; in other circles it was characterized as an

adventure in “socialism, communism and devilism” devised by “the

professors with their books, the socialists with their schemes,” and “the

anarchists with their bombs.”

These, of course, were not charges of impressive legal weight, and when

the validity of the tax reached the Supreme Court in Pollock v. Farmers’ Loan

& Trust Co.,

9

the tax was challenged principally on three constitutional

grounds: (1) that it constituted a direct tax which did not meet the

constitutional requirement that such measures be apportioned among the

states on the basis of population;

10

(2) that because it exempted incomes

below $4,000, it violated the constitutional requirement that taxes be

uniform throughout the United States;

11

and (3) that it impinged on the

rights of state and local governments by taxing the interest on obligations

issued by these bodies.

12

Although the Supreme Court previously had

indicated that direct taxes included only land and capitation taxes,

13

and had

upheld the constitutionality of the Civil War income taxes,

14

it nonetheless

ultimately concluded in Pollock that taxes on income from real and personal

property were direct taxes within the meaning of the Constitution, that the

Federal Government could not validly tax the obligations of state and local

governments, and that the 1894 tax was so infected with unconstitutionality

that it was totally void.

15

The Pollock decision has been severely criticized by

students of constitutional law and others; nevertheless, it had the effect of

delaying general income taxation in the United States for almost two

decades.

The beginning of the twentieth century witnessed important social and

political changes in the United States. Public attention was increasingly

focused on the abuses of economic power characteristic of the time.

Extreme poverty among workers, exploitation of labor generally and child

labor in particular, increasing concentration of wealth, and monopolistic

and corrupt practices of corporate giants were all issues that were colorfully

ventilated by a new form of journalism, “muckraking.” Powerful new

9

157 U.S. 429, rehearing 158 U.S. 601 (1895).

10

U.S. CONST. art. I, § 9.

11

U.S. CONST. art. I, § 8, cl. 1.

12

Cf. U.S. CONST. Amend. X.

13

Hylton v. United States, 3 U.S. (3 Dall.) 171, 174 (1796).

14

Springer v. United States, 102 U.S. 586 (1880).

15

The Court did not pass on the question of whether the uniformity clause was

violated. Later, it was established that uniformity meant geographic uniformity

rather than rate uniformity—rates could be progressive so long as the same rates

applied equally throughout the nation. Knowlton v. Moore, 178 U.S. 41 (1900).

6 The United States Tax Court – An Historical Analysis

political leaders emerged, such as Robert LaFollette and Theodore

Roosevelt, who were sensitive to these issues. These events had an impact

on the question of income taxation and gave it a new respectability. Perhaps

the best illustration of this rested in remarks of President Roosevelt in 1906

on the occasion of the laying of the cornerstone of a new office building for

the House of Representatives.

[The President] made a flamboyant Fourth-of-July speech for ten

minutes, an uplift speech for fifteen, skinned the muckrakers within

an inch of their lives, and delivered a few light taps on Democratic

ribs. The mouths of the eminent Republican magnates were spread

in smiles reaching from ear to ear. They were having the time of

their lives, when suddenly, without any connection whatever with

anything he had said, apropos of nothing, he declared vehemently

for both a graduated income tax and a graduated inheritance tax.

The Democrats were jubilant and applauded hilariously, while the

smiles froze on the faces of the Republicans. They would not have

been more astonished if he had struck them betwixt the eyes with a

maul. They had to pinch themselves to see if they were awake. The

President seemed to be delighted with the sensation he had created

and the consternation he had wrought among Republican statesmen.

Their curses on him for that speech were not only deep, but loud.

16

Roosevelt continued to make statements supporting a graduated income

tax, but took little if any affirmative action to secure its adoption.

Nevertheless, the fact that a Republican President would even

philosophically support such a measure did much to defuse the temper of

the debate—one could hardly accuse the President of being a “bomb

throwing anarchist.” Furthermore, Roosevelt’s successor, William Howard

Taft, gave campaign speeches expressing support for such a tax when

demanded by revenue needs. In his view an income tax could be devised

which would be constitutional notwithstanding the Pollock decision. As

with Roosevelt, Taft did not initiate an income tax program and it has been

suggested that his public enthusiasm for the tax was manufactured as a

shrewd ploy to steal the thunder of his Democratic rival, William Jennings

Bryan, who was an outspoken advocate of income taxation.

Yet, it was during the Taft Administration that the seed of the modern

income tax was planted. This is ironic because during this period

Republicans, traditionally hostile to the measure, controlled not only the

White House but the House of Representatives and the Senate as well. The

irony is explained by the character of the congressional Republican

delegation which had changed from earlier years. Midwestern Republican

16

1 CHAMP CLARK, MY QUARTER CENTURY OF AMERICAN POLITICS 440

(1920).

The Origins of the Tax Court 7

progressives such as LaFollette and Cummins had recently entered the

Senate and forged an alliance with Democrats favorable to income taxation.

During the Senate consideration of the Payne-Aldrich Tariff Bill, this

coalition actively pressed for inclusion of a general graduated income tax.

The Republican hierarchy opposed the measure but could not control the

insurgents within their party. Ultimately, in an effort to save the tariff

legislation and also to prevent an open breach within the Republican party,

President Taft effected a grudging compromise. Taft had come to change

his mind on the question of whether Pollock would be overruled by the

Supreme Court and felt that the more prudent course was to amend the

Constitution to permit an income tax without apportionment. A proposal

for such an amendment constituted one element of his compromise plan.

The second element of the plan was the immediate enactment of a

corporation excise tax measured by corporate income. Taft felt that such a

tax would not be a direct tax and could withstand constitutional attack.

Although the Taft proposal was opposed by a few diehard advocates of an

immediate general income tax, it was reluctantly backed by the conservative

Republicans who saw it as the lesser of two evils. This support, along with

the approval of the moderate pro-income tax forces, was sufficient for

passage.

17

The corporation income tax, which was 1% of taxable income in excess

of $5,000, was upheld by the Supreme Court in 1911.

18

As anticipated by

Taft, the Court distinguished the Pollock case on the ground that the levy

was indirect since it was imposed on the privilege of doing business as a

corporation and not on the income from property. That the tax was

measured by income from property was not a constitutional defect, even

though a tax imposed directly on such income might be invalid.

By 1913, two thirds of the states had approved the Sixteenth

Amendment, which provides:

The Congress shall have power to lay and collect taxes on incomes,

from whatever source derived, without apportionment among the

several States, and without regard to any census or enumeration.

The debate concerning the Amendment was a lively one, but approval

was assured because of the new respectability of the income tax and

because the more numerous and less wealthy elements of society believed

such a tax would shift a greater portion of the tax burden onto the wealthy.

The arguments against the proposed amendment, that it would permit the

taxation of state and local bonds and that the income tax would be difficult

to administer and produce a nation of liars, were of insufficient persuasive

force to stanch the flow of popular support.

17

Act of August 5, 1909, ch. 6, § 38, 36 Stat. 112.

18

Flint v. Stone Tracy Co., 220 U.S. 107 (1911).

8 The United States Tax Court – An Historical Analysis

One month after final ratification of the income tax amendment,

Woodrow Wilson assumed the Office of President. Although Wilson was

not an advocate of free trade, he was decidedly hostile to what he saw as the

excesses of the existing tariff system, both in its adverse effect on

competition and in its use as an indirect tax on consumption. Similar

sentiments were commonplace in Congress. By the fall of 1913, legislation

had been adopted substantially cutting the tariff schedules and, more

importantly, imposing a general income tax to balance the lost customs

revenues.

19

Conservatives actively opposed adoption of the income tax, but

it was an idea whose time had come (for the third time) and the anti-tax

forces did not even succeed in their efforts to eliminate progressive rates.

They did, however, have some success in moderating the rates of tax. The

1913 legislation provided a 1% normal tax on taxable income of individuals

in excess of $3,000 ($4,000 in the case of married persons) plus a graduated

surtax.

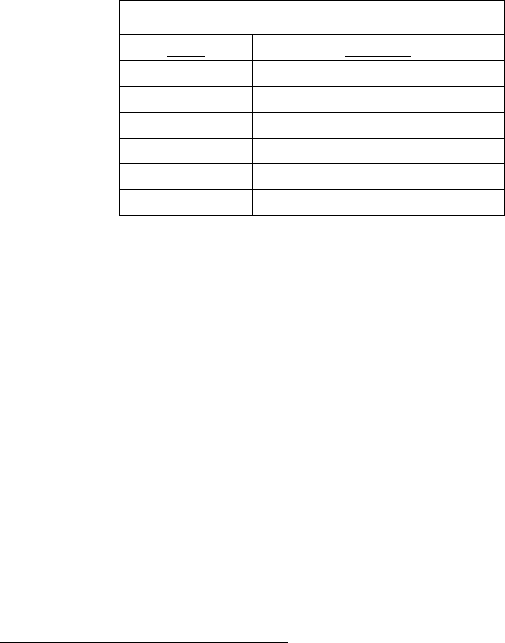

20

Surtax

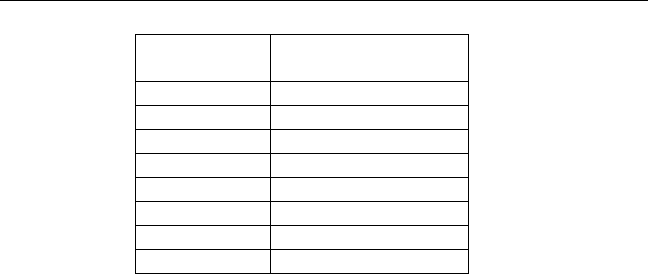

Rate

Income

1%

$20,000 – $50,000

2%

$50,000 – $75,000

3%

$75,000 – $100,000

4%

$100,000 – $250,000

5%

$250,000 – $500,000

6%

Over $500,000

Thus, the maximum rate of tax on individuals was 7% on taxable

income above $500,000. Corporations were subject to a flat rate of 1% on

all their taxable income.

21

In addition to providing relatively low rates, which produced only $28

million of revenue in the first year, the 1913 tax also contained a generous

exemption, with the result that for 1913 only 358,000 individual income tax

returns were filed in a nation with a population of 97 million. However, the

upcoming war was to change drastically the character of the income tax.

In 1914, World War I broke out in Europe. Initially committed to a

policy of neutrality, President Wilson by the spring of 1917 was compelled

to ask Congress for a declaration of war against Germany. The war had a

staggering impact on the financial affairs of the United States. One of the

first casualties was the customs receipts that soon dwindled as a result of

trade reduction. This was a significant setback to a nation that in 1913 still

derived almost one-half of its government revenues from these sources.

19

Act of October 3, 1913, ch. 16, 38 Stat. 114.

20

Id. §§ II(A), (C), 38 Stat. 166, 168.

21

Id. § II(A)(1), 38 Stat. 166.

The Origins of the Tax Court 9

The diminution in these revenues was felt as early as 1914 and resulted in

the enactment of the War Revenue Bill of 1914,

22

which levied various

internal excise taxes to make up for the lost revenue.

Of course, even more significant was the staggering growth of

expenditures required of a nation at war. The cost of operating the

Government grew from approximately $700 million in each of the years

1913–16, to $2 billion in 1917, $13 billion in 1918 and $19 billion in 1919.

For 1914 there was a deficit of $400,000; for 1919, the deficit was $13

billion.

Although Wilson’s hopes for neutrality were not finally extinguished

until 1917, he foresaw the possibility of American involvement as early as

1915, and toward that end the United States commenced a military

expansion program in 1916. The income tax was to play an increasingly

important role in financing both the military preparedness program and the

costs of subsequent entry into the war.

Within a period of three years, the Revenue Acts of 1916,

23

1917,

24

and

1918

25

(the latter being enacted in 1919 but made retroactive to January 1,

1918) escalated the income tax on individuals to a normal tax computed as

follows:

Additionally, there was imposed a surtax ranging from 1% on income in

excess of $5,000 to 65% on income in excess of $1,000,000.

26

Thus, the

maximum rate was 77%, which was 1,100% greater than the maximum rate

prevailing from 1913–1916. Corporate tax rates also advanced

spectacularly. By 1918, corporations were paying a tax of 12% on net

income,

27

plus a profits tax escalating from 30% to 80% of so-called excess

profits or war profits.

28

The excess profits tax was introduced by the Act of March 3, 1917,

29

just one month prior to the declaration of war against Germany. Although

the March 3 legislation was soon to be superseded by the War Revenue Act

22

Act of October 22, 1914, ch. 331, 38 Stat. 745.

23

Revenue Act of 1916, ch. 463, 39 Stat. 756.

24

War Revenue Act of 1917, ch. 63, 40 Stat. 300.

25

Revenue Act of 1918, ch. 18, 40 Stat. 1057.

26

Revenue Act of 1918, ch. 18, § 211, 40 Stat. 1062.

27

Id. § 230(a)(1), 40 Stat. 1076.

28

Id. § 301(a), 40 Stat. 1088.

29

Ch. 159, § 201, 39 Stat. 1000.

Normal Tax

Rate

Income

6 %

$2,000 – $6,000

12 %

Over $6,000

10 The United States Tax Court – An Historical Analysis

of 1917, enacted October 3, 1917,

30

the excess profits tax itself persisted

until it was repealed by the Revenue Act of 1921.

31

It was later to reappear

during World War II and the Korean War. The tax had the dual purpose of

curbing war profiteering and raising revenue from those best able to afford

to pay a larger share of tax. The tax was a complicated one in that it

required the measurement of excess profits. Whether such profits were

measured by income in excess of a percentage of capital

32

or by profits in

excess of those from a prior base period,

33

the determination created many

uncertainties and disputes.

34

These difficulties were to play an important

part in providing the impetus for the creation of the Board of Tax Appeals.

The effect of the wartime revenue measures on the importance of

income taxes was impressive. Government revenue rose from $780 million

in 1916 to $6.7 billion in 1920. As a result of the wartime revenue acts,

receipts from income and profits taxes over this same period rose from

$125 million to $3.9 billion. In 1916, they represented 16 percent of

receipts; by 1920, this percentage had risen to 55 percent.

These spectacular increases were accompanied by a corresponding, and

universally recognized, increase in the complexity of the law.

35

One

indication of this appeared in the increased length of the succeeding acts.

Excluding the tariff and excise provisions, the 1913 Act took up only 16

pages in the Statutes at Large, the 1916 Act took up 22 pages, and the 1918

Act required 53 pages. This increase in statutory length mirrored the

substantive evolution of the tax law. Several important and complicating

provisions were added by the 1916 legislation: the term “dividend” was

defined for the first time;

36

taxpayers were permitted to report income on a

method other than the cash method of accounting;

37

losses incurred in a

transaction for profit were made deductible even though not incurred in a

trade or business;

38

detailed statutory treatment was provided for

nonresident aliens;

39

the income of estates and trusts was subjected to tax

30

Ch. 63, 40 Stat. 300.

31

Revenue Act of 1921, ch. 136, § 1400(a), 42 Stat. 320.

32

Revenue Act of 1918, ch. 18, §§ 301, 312, 40 Stat. 1088, 1091 (relating to

excess profits tax).

33

Id. §§ 301, 311, 40 Stat. 1088, 1090 (relating to war profits tax).

34

Hearings Pursuant to S. Res. 168 Before the Senate Select Comm. on Investigation of the

Bureau of Internal Revenue, 68th Cong., 1st Sess., pt. 1 at 132 (1924) (statement of

David H. Blair, Comm’r of Int. Rev.) [hereinafter cited as Senate Select Comm.

Hearings].

35

See, e.g., Senate Select Comm. Hearings, supra note 34, pt. 1 at 120–21 (1924)

(statement of David H. Blair, Comm’r of Int. Rev.); Turner, supra note 2, at 32.

36

Revenue Act of 1916, ch. 463, § 2(a), 39 Stat. 757.

37

Id. § 8(g), 39 Stat. 763.

38

Id. § 5(a), 39 Stat. 759. It was later held that no such losses were allowed

under the 1913 Act. Mente v. Eisner, 266 F. 161 (2d Cir. 1920).

39

Ch. 463, § 6, 39 Stat. 760.

The Origins of the Tax Court 11

for the first time;

40

and the class of organizations exempt from tax was

substantially increased.

41

The most important change from earlier law

effected by the 1917 Act was, of course, the addition of the excess profits

tax.

42

The Act provided for the filing of consolidated returns for excess

profits tax purposes,

43

which added some complexity. The 1918 Act also

contained many important amendments: consolidated returns were

authorized for both income and profits tax purposes;

44

substantial

modifications were made in the profits tax;

45

provision was made for the

nonrecognition of gain in connection with corporate reorganizations;

46

authority was given to the Bureau to require the taking of inventories;

47

a

provision for the carryover of net operating losses was added;

48

and a

special amortization deduction was authorized for war facilities.

49

With the end of the war and the return of surplus revenues, pressure for

reduction in the income taxes became overwhelming. In addition to

eliminating the excess profits tax, the Revenue Act of 1921 substantially

reduced the individual and corporate income tax rates.

50

Even with the

40

Id. § 2(b), 39 Stat. 757.

41

Id. § 11, 39 Stat. 766.

42

War Revenue Act of 1917, ch. 63, § 201, 40 Stat. 303.

43

Revenue Act of 1921, ch. 136, § 1331, 42 Stat. 319 (construing provisions of

Revenue Act of 1917).

44

Revenue Act of 1918, ch. 18, § 240(a), 40 Stat. 1081.

45

See H.R. REP. NO. 65-767, at 15–21 (1918); S. REP. NO. 65-617, at 11–15

(1918).

46

Revenue Act of 1918, ch. 18, § 202(b), 40 Stat. 1060.

47

Id. § 203, 40 Stat. 1060.

48

Id. § 204, 40 Stat. 1060.

49

Id. §§ 214(a)(9), 234(a)(8), 40 Stat. 1067, 1078.

50

The 1921 Act provided a normal tax on married individuals (ch. 136, §§ 210,

216(c), 42 Stat. 233, 242) as follows:

Normal Tax

Rate

Income

4%

$2,000 – $6,000

8%

Over $6,000

In the case of a single person, these rates were 4% on income from $1,000–

$5,000, and 8% on income in excess of $5,000. In the case of a married couple

with income of not more than $5,000, the exemption was $2,500 instead of $2,000.

The individual surtax rates ranged from 1% of income over $6,000 to 50% of

income in excess of $200,000. Ch. 136, § 211, 42 Stat. 233. For the transition year

1921, these rates ranged from 1% on income in excess of $5,000 to 65% on income

in excess of $1 million.

Although the tax rate on corporations was increased from 10% to 12½% for

years following 1921 (§ 230, 42 Stat. 252), a $2,000 exemption (§ 236(b), 42 Stat.

257) and the elimination of the excess profits tax resulted in corporations being

12 The United States Tax Court – An Historical Analysis

reduction of rates in 1921, and the later reductions that were to take place

during the 1920’s, the income tax had firmly established itself as the

principal device for financing government activities. Since 1918, receipts

from the income (individual and corporate) and excess profits taxes have

rarely yielded less than half of annual government receipts; in some years

they have yielded considerably more than half.

51

B. Inadequacy of Preexisting Adjudicative Institutions

The income and excess profits taxes of the World War I period placed

an enormous strain on the Bureau of Internal Revenue and, to a lesser

extent, on the federal courts. In the first place, the taxes were considerably

more complicated than any other revenue device previously utilized by the

Federal Government. This problem was recognized at the very beginning

of the modern income tax. A friend who complained to Senator Elihu

Root of the complexities of the 1913 Act elicited the following response:

I guess you will have to go to jail. If that is the result of not

understanding the Income Tax Law I shall meet you there. We shall

have a merry, merry time, for all of our friends will be there. It will

be an intellectual center, for no one understands the Income Tax

Law except persons who have not sufficient intelligence to

understand the questions that arise under it.

Even the income tax of the Civil War period, while much simpler than the

later measures, was not without its complexities. For example, Abraham

Lincoln, an able lawyer of his day, overpaid his 1864 income tax by $1,250,

which sum was ultimately refunded to his estate in 1872.

The excess profits tax was, if anything, even more complicated than the

income tax. Dr. Thomas S. Adams, a distinguished political economist,

professor at Yale University, adviser to the Treasury Department, and

fervent supporter of income taxation, urged repeal of the profits tax in 1921

on the ground that its continuation would inevitably lead to the breakdown

of tax administration and the repeal of the income tax as well.

In addition to their complexity, the income taxes of the World War I

period affected vast numbers of people. The lowering of exemptions

resulted in a staggering increase in the number of returns filed. Until 1917,

subject to less overall tax than under the 1918 Act. See supra notes 27–28 and

accompanying text.

51

However, in recent years, social insurance taxes have represented an

increasing share of federal revenue, reaching as high as 42.3% in 2010. See S

TAFF

OF THE

JOINT COMM. ON TAX’N, OVERVIEW OF THE FEDERAL TAX SYSTEM AS IN

EFFECT FOR 2012, JCX-18-12, app. A-3 (Comm. Print 2012).

The Origins of the Tax Court 13

the number of income tax returns filed by individuals did not exceed

450,000 for any single year. In 1917, this number increased to 3.5 million

and by 1920 more than 7 million individual income tax returns were being

filed. Not until 1925 did the number of filings fall below 6 million.

Finally, the experience of the last century has demonstrated that,

regardless of the detail provided, it is impossible to draft an income tax

statute that clearly provides for all factual circumstances. Accordingly, in

addition to the taxing statute, an income tax system requires a sophisticated

administrative body to collect the tax and provide interpretations of the

statute. As shall be seen, such a body cannot be built overnight.

1. Dilemma of the Bureau

Revenue legislation in the United States dates back almost as far as the

formation of the Republic. The first July 4th after adoption of the

Constitution was marked by the enacting of a duty on goods, wares, and

merchandise imported into the United States.

52

This enactment even

preceded establishment of the Treasury Department.

53

Numerous revenue

measures followed, but until the Civil War these were almost exclusively

tariffs. Only during two brief periods was there resort to internal taxation:

1791–1802 and 1813–1817.

54

This sparing use of internal taxation seems to

have been consistent with the intention of the framers of the Constitution,

who felt that such techniques should be utilized only in exceptional

circumstances,

55

reminiscent as they were of the hated excises imposed in

the pre-revolutionary period by the British Parliament. Moreover, internal

taxation was not popular with the public and the first imposition of internal

excises on distilled spirits gave rise to an insurrection by Pennsylvania

farmers in the summer of 1794.

During each of the early periods of internal taxation, an office of

Commissioner of the Revenue was created to administer the levies.

However, the office was abolished each time the internal duties were

repealed.

56

The modern Internal Revenue Service traces its lineage to the

legislation imposing the income tax of 1862 and the various other internal

taxes that were established to finance the Union’s war effort.

57

The first

Commissioner appointed under the 1862 legislation, George Boutwell,

worked industriously to establish the organization, regulations and forms

52

Act of July 4, 1789, ch. 2, § 1, 1 Stat. 24.

53

Act of September 2, 1789, ch. 12, 1 Stat. 65.

54

For a detailed account of these measures, see BUREAU OF INTERNAL

R

EVENUE, THE WORK AND JURISDICTION OF THE BUREAU OF INTERNAL

R

EVENUE 5–28 (1948) [hereinafter cited as BUREAU OF INTERNAL REVENUE].

55

T HE FEDERALIST NO. 35, at 93-95, 124–25 (R.P. Fairfield ed. 1966).

56

B UREAU OF INTERNAL REVENUE, supra note 54.

57

Act of July 1, 1862, ch. 119, § 1, 12 Stat. 432.

14 The United States Tax Court – An Historical Analysis

necessary for tax administration. Within six months, the Bureau had grown

from a staff of one (Mr. Boutwell) to an organization of almost 4,000

employees.

58

In view of the enormous responsibilities suddenly thrust upon the

organization, it was not surprising that in its early years the Bureau was far

from an unqualified success. The United States Revenue Commission

established in 1865 to study the raising of tax revenues and the efficiency of

tax administration concluded that “in point of organization and

administration, . . . [the Bureau] is very far from what it should be.”

59

The

cited weaknesses of the Bureau included the following: lack of policy

making authority; inadequate pay; appointments based on patronage rather

than ability; and political interference with its decisions.

60

The income tax of the Civil War period was repealed effective 1872,

61

and most of the other internal taxes imposed to finance the War were

repealed by 1877. Nevertheless, the Bureau continued in existence to

administer the remaining internal taxes and those thereafter enacted, such

as the taxes on alcoholic beverages and tobacco.

62

Additionally, it was

given charge of various non-revenue regulatory measures such as the

bounty for United States sugar producers, the certification of Chinese

laborers, and the taxes on opium and oleomargarine.

The imposition of the corporation income tax in 1909 and the general

income tax in 1913 added new duties to the Bureau, and created a

concomitant growth in its size. But the changes wrought by the early

income tax acts were small compared to those of the World War I revenue

legislation. As a result of the introduction of the excess profits tax and the

expansion of the income tax, there was a more than ten-fold increase in the

number of returns filed. The Bureau was buried under a mountain of

paper. Because it was the policy of the Bureau to review virtually each

return filed,

63

and because the laws under which the returns were filed were

considerably more complicated than any previous tax measures,

monumental problems of administration arose. The turmoil that ensued

persisted for a decade.

The years 1917 through 1919 witnessed almost complete paralysis of the

Bureau. The personnel of the Washington office increased from 585 in

58

I NTERNAL REVENUE SERVICE, INCOME TAXES 1862–1962: A HISTORY OF

THE INTERNAL REVENUE SERVICE 7 (1962) [hereinafter cited as INTERNAL

R

EVENUE SERVICE].

59

Id. at 11.

60

Id.

61

Act of July 14, 1870, ch. 255, § 6, 16 Stat. 257.

62

See Senate Select Comm. Hearings, supra note 34, pt. 1 at 120 (1924)

(statement of David H. Blair, Comm’r of Int. Rev.); I

NTERNAL REVENUE SERVICE,

supra note 58, at 12.

63

See 1919 COMM’R OF INT. REV. REP. 18.

The Origins of the Tax Court 15

1917 to 4,088 in 1919,

64

but few of the Bureau’s staff were equipped with

the special legal, accounting, and engineering background necessary to

assess the accuracy of millions of the returns filed.

65

Particularly

troublesome were questions of property valuation on which depended

deductions for depreciation, amortization, and depletion, and on which

invested capital was computed for excess profits tax purposes.

66

According

to some, there were not sufficient trained people in the entire country to